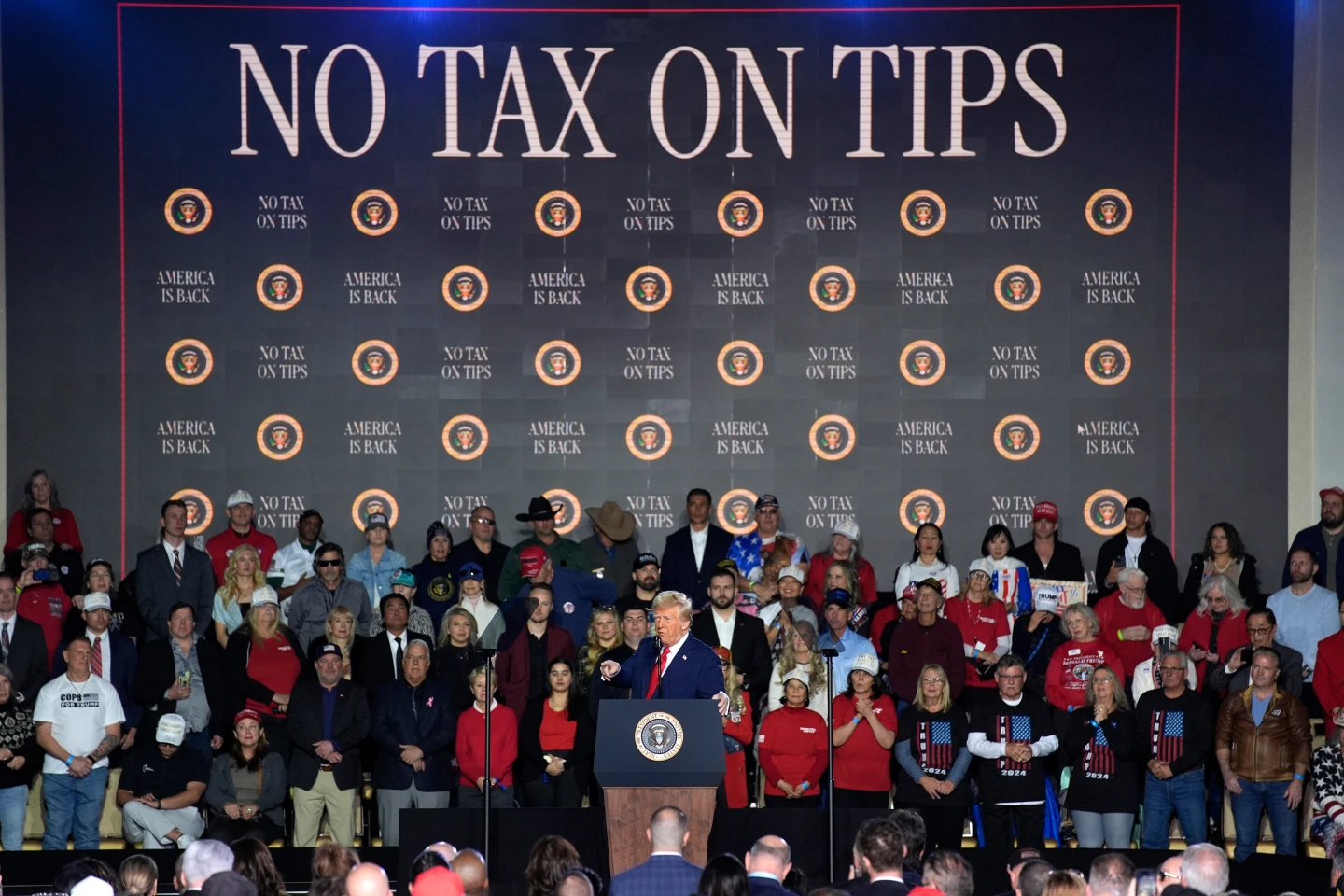

As the new year approaches, legislators across the United States will grapple with decisions regarding the adoption of tax breaks proposed by President Donald Trump's administration. These tax incentives encompass deductions for tips, overtime wages, and certain loan interests, aiming to provide financial relief for individuals and businesses alike.

In many states, federal tax changes will automatically translate to state income tax unless expressly rejected by the legislature. In contrast, states with different tax frameworks may only incorporate such changes if they actively decide to embrace them. This discrepancy places pressure on lawmakers to swiftly address these proposals as they convene.

States choosing to adopt Trump’s tax cuts could save hundreds of millions of dollars for their constituents. However, many are hesitating due to existing financial strains from rising costs associated with Medicaid and SNAP food aid obligations included in the broader federal legislation.

Most states commence their annual legislative sessions in January, necessitating quick action to update tax regulations. A delay might defer these changes to the 2026 tax year, offering less urgency but potentially leaving many taxpayers without the impending relief.

While some states have already initiated discussions regarding these tax incentives, overall sentiment appears cautious. Legislators are particularly wary of how these decisions can create unforeseen financial burdens on state revenues.

Treasury Secretary Scott Bessent has pushed for immediate conformity to federal tax cuts, criticizing some states for engaging in “political obstructionism.” However, state financial analysts urge caution, suggesting that the implementation of such tax breaks needs to be weighed against potential revenue losses and economic implications.

Michigan stands out as the only state to have adopted these tax deductions for tips and overtime, while others continue to weigh the financial fallout of conformity to federal tax policy. As lawmakers evaluate the merits of these changes amidst their unique budgetary landscapes, the outcome of these discussions could significantly reshape fiscal policy across the nation.